All Categories

Featured

Table of Contents

Eliminating agent payment on indexed annuities allows for dramatically greater illustrated and real cap rates (though still considerably reduced than the cap prices for IUL policies), and no doubt a no-commission IUL plan would certainly press detailed and real cap prices higher. As an aside, it is still feasible to have an agreement that is extremely abundant in representative settlement have high very early money abandonment worths.

I will acknowledge that it goes to the very least theoretically feasible that there is an IUL plan available issued 15 or two decades ago that has actually delivered returns that transcend to WL or UL returns (more on this below), however it is very important to much better understand what an ideal comparison would certainly involve.

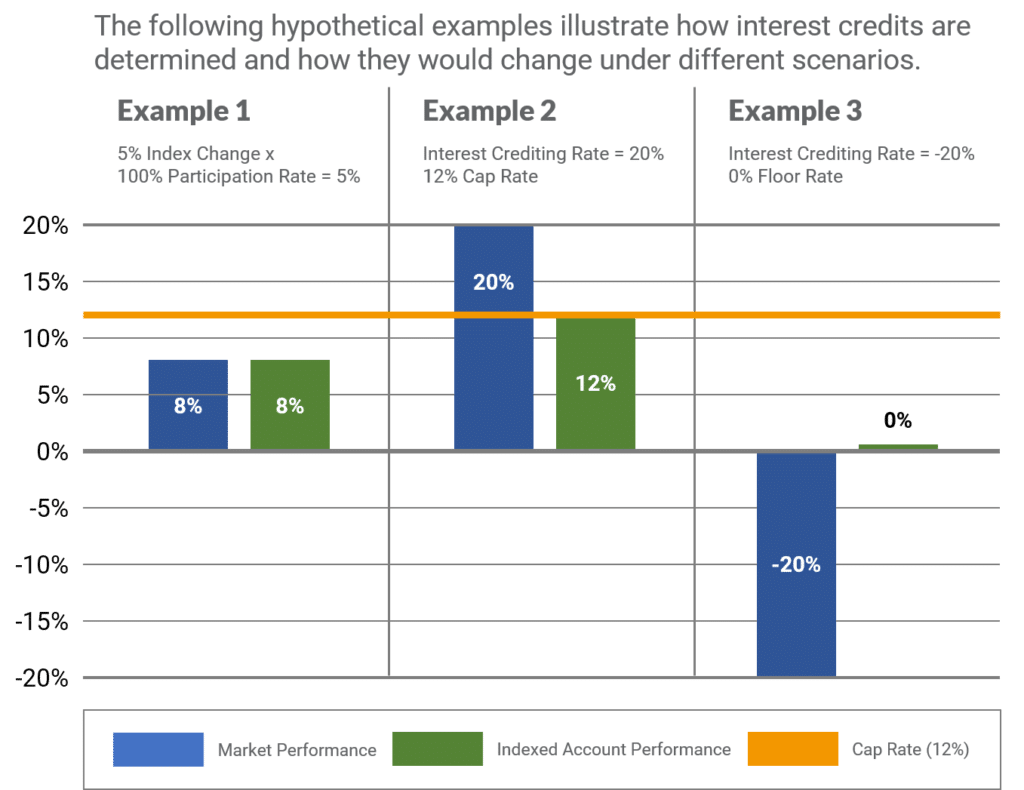

These plans generally have one lever that can be evaluated the company's discernment yearly either there is a cap rate that defines the optimum attributing price in that specific year or there is an involvement rate that specifies what percent of any kind of favorable gain in the index will certainly be passed along to the policy because specific year.

And while I normally agree with that characterization based upon the auto mechanics of the plan, where I differ with IUL advocates is when they define IUL as having exceptional returns to WL - guaranteed universal life insurance cost. Several IUL supporters take it an action further and factor to "historic" information that appears to sustain their insurance claims

There are IUL policies in existence that carry even more danger, and based on risk/reward principles, those policies need to have higher expected and real returns. (Whether they actually do is an issue for serious argument but companies are utilizing this technique to aid justify greater detailed returns.) Some IUL plans "double down" on the hedging approach and examine an additional charge on the plan each year; this fee is then made use of to enhance the options budget plan; and after that in a year when there is a favorable market return, the returns are amplified.

Iul For Retirement Income

Consider this: It is possible (and as a matter of fact likely) for an IUL policy that standards an attributed price of say 6% over its first one decade to still have a total adverse price of return during that time as a result of high costs. A lot of times, I discover that agents or consumers that boast about the performance of their IUL plans are puzzling the attributed rate of return with a return that properly mirrors all of the plan bills too.

Next we have Manny's inquiry. He claims, "My buddy has been pushing me to get index life insurance coverage and to join her business. It looks like an Online marketing.

Insurance salespersons are not bad individuals. I'm not suggesting that you would certainly despise on your own if you stated that. I claimed I utilized to do it, right? That's exactly how I have some insight. I used to offer insurance at the beginning of my profession. When they market a premium, it's not unusual for the insurer to pay them 50%, 80%, even often as high as 100% of your first-year premium.

It's hard to sell because you obtained ta always be looking for the following sale and going to discover the next individual. It's going to be difficult to find a whole lot of gratification in that.

Let's chat regarding equity index annuities. These points are popular whenever the markets are in an unstable duration. You'll have surrender periods, usually 7, ten years, perhaps also beyond that.

Is An Iul A Good Investment

Their abandonment periods are massive. That's how they know they can take your money and go totally invested, and it will be fine since you can not obtain back to your cash until, once you're into seven, ten years in the future. That's a long-term. Regardless of what volatility is taking place, they're most likely mosting likely to be great from a performance point ofview.

There is no one-size-fits-all when it revives insurance. Obtaining your life insurance plan right takes into account a number of variables. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your hectic life, economic independence can feel like an impossible goal. And retirement might not be leading of mind, because it appears up until now away.

Pension plan, social protection, and whatever they would certainly taken care of to conserve. It's not that very easy today. Fewer companies are providing traditional pension strategies and numerous companies have minimized or stopped their retired life strategies and your ability to depend entirely on social security remains in inquiry. Also if benefits have not been decreased by the time you retire, social protection alone was never planned to be enough to pay for the way of living you want and are entitled to.

Cost Of Universal Life Insurance

/ wp-end-tag > As component of an audio economic approach, an indexed global life insurance coverage policy can assist

you take on whatever the future brings. Before committing to indexed global life insurance policy, below are some pros and cons to think about. If you pick a good indexed global life insurance coverage plan, you might see your money value expand in worth.

If you can access it early, it may be advantageous to factor it into your. Given that indexed universal life insurance policy needs a certain level of risk, insurer tend to maintain 6. This sort of strategy additionally provides. It is still ensured, and you can readjust the face amount and bikers over time7.

Generally, the insurance firm has a vested rate of interest in doing much better than the index11. These are all variables to be taken into consideration when picking the best type of life insurance policy for you.

Nonetheless, considering that this kind of plan is extra intricate and has an investment part, it can often come with greater costs than other policies like entire life or term life insurance. If you do not believe indexed global life insurance coverage is appropriate for you, right here are some choices to consider: Term life insurance is a momentary plan that normally supplies protection for 10 to 30 years.

Linked Life Insurance

Indexed global life insurance coverage is a sort of plan that supplies more control and flexibility, along with higher cash worth development possibility. While we do not offer indexed global life insurance policy, we can offer you with more details regarding whole and term life insurance policy plans. We suggest discovering all your options and talking with an Aflac agent to find the very best suitable for you and your family members.

The remainder is included to the cash money value of the policy after charges are subtracted. While IUL insurance policy may prove beneficial to some, it's important to recognize exactly how it functions prior to acquiring a policy.

{kind=link}

Table of Contents

Latest Posts

Ul Mutual Company

Universal Indexed Life Insurance

Death Benefit Option 1

More

Latest Posts

Ul Mutual Company

Universal Indexed Life Insurance

Death Benefit Option 1